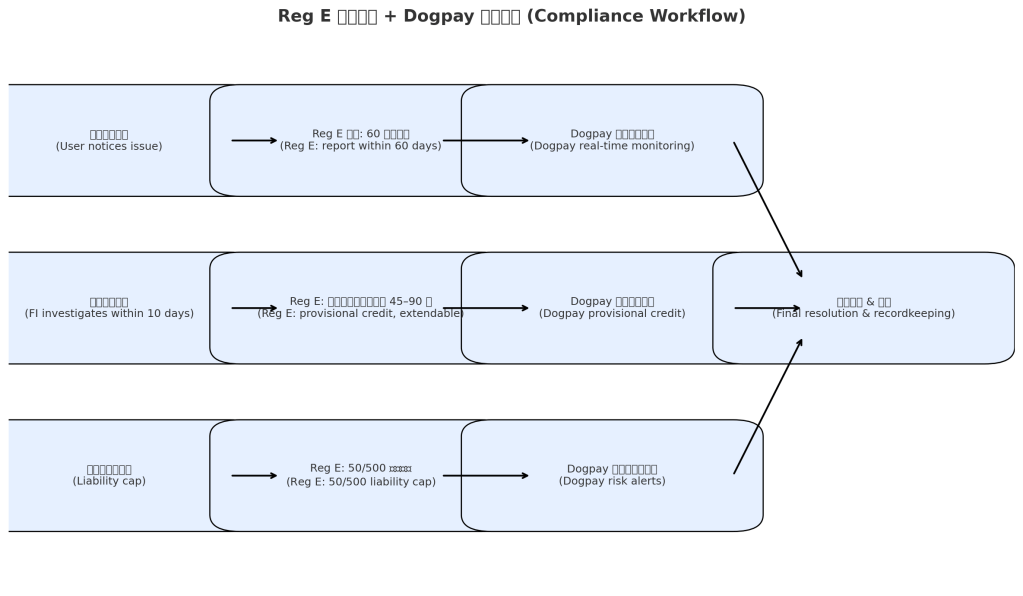

Regulation E, issued under the Electronic Fund Transfer Act (EFTA), establishes consumer protection standards for electronic fund transfers (EFTs), such as ATM withdrawals, POS purchases, ACH direct deposits/payment, remittance transfers, and government benefits disbursement. It sets the rules for error resolution, fee disclosures, consumer liability, and preauthorized transfers.

Core Elements of Regulation E

- Error Reporting & Investigation TimelineConsumers have 60 days from statement date to report errors. Financial institutions must investigate within 10 business days; with provisional credit given, the period may extend to 45–90 days depending on context.

- Consumer Liability CapsIf timely reported, consumer liability for unauthorized EFTs is capped at $50; late reporting can increase liability up to $500 or more.

- Mandatory TransparencyInstitutions must clearly disclose all EFT service terms beforehand—including rights, fee schedules, and error resolution procedures.

How Dogpay Elevates Regulation E Compliance into User-Centric Solutions

Dogpay, a cutting-edge digital payments and identity platform, turns Regulatory E’s requirements into seamless, value-added user experiences:

- Real-Time Error Detection and Auto-Initiated Dispute Process

- Dogpay monitors transactions in real time. Suspicious activity triggers an automated dispute, aligning with Reg E’s timing protocols and easing customer effort.

- Clear Risk Communication

- The interface clearly advises users of liability thresholds when reporting promptly, encouraging quick action and minimizing user exposure.

- Streamlined Disclosure Integration

- All Reg E-required disclosures are embedded into initial service onboarding, ensuring users understand their rights from the outset.

- Fast Provisional Credit System

- Dogpay automatically issues provisional refunds upon error reports, protecting user funds while investigation proceeds—complying with Reg E’s extended investigation allowances.

- Comprehensive Recordkeeping and Audit Trail

- Every transaction, dispute, credit, and resolution is logged. Records are exportable and maintained for regulatory retention periods (usually two years or more).